Vietnam Q1 2026 economic outlook

May 11, 2026

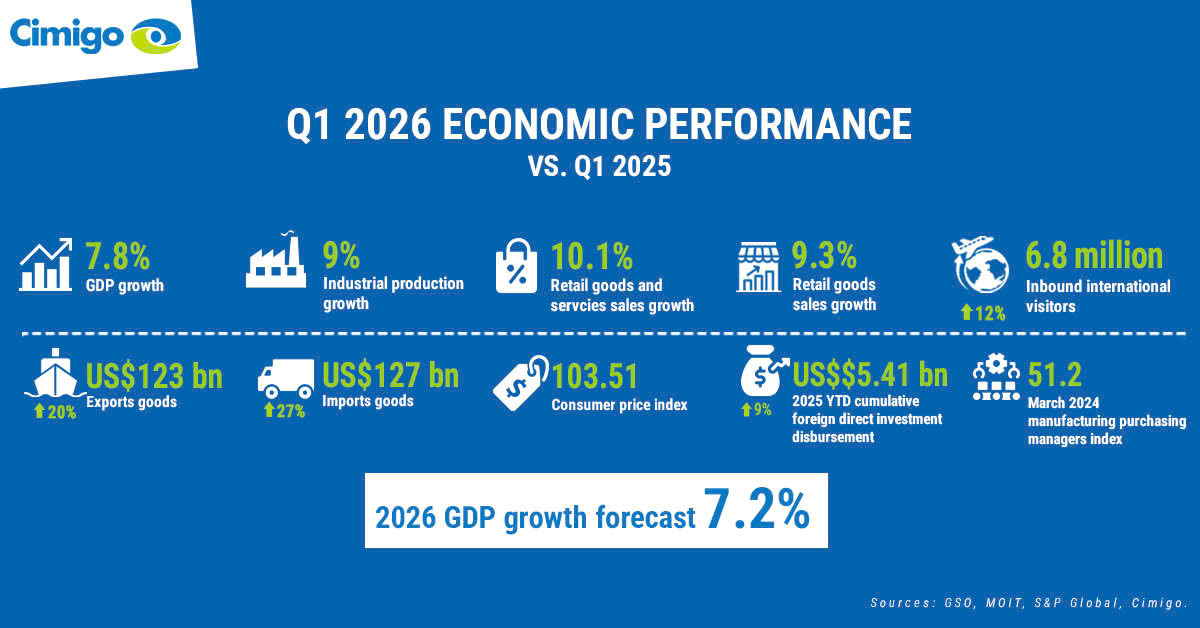

Vietnam Q1 2026 economic outlook: strong growth, rising pressure, falling confidence Vietnam Q1

Vietnams Economic Recovery Post-Covid

This article looks at navigating Vietnams economic recovery post-Covid. Vietnam is open for business again in October 2021, after four months of economic interruptions in efforts to protect health and save lives. The mid-term prospects for Vietnam’s economic recovery are strong.

However, consumer spending will only return to pre-pandemic 2019 levels after 18 to 24 months. This pandemic will force a sharp drop in discretionary expenditure. There will be GDP growth of approximately 2.4% in 2021. This is the lowest level since 1986 which recorded a 2.3% growth. It will be less than 2020 which recorded 2.9% and in sharp contrast to the 7.0% growth achieved in 2019. Consumer dynamism and economic growth will rebound unabated by mid-2023.

6 minute read.

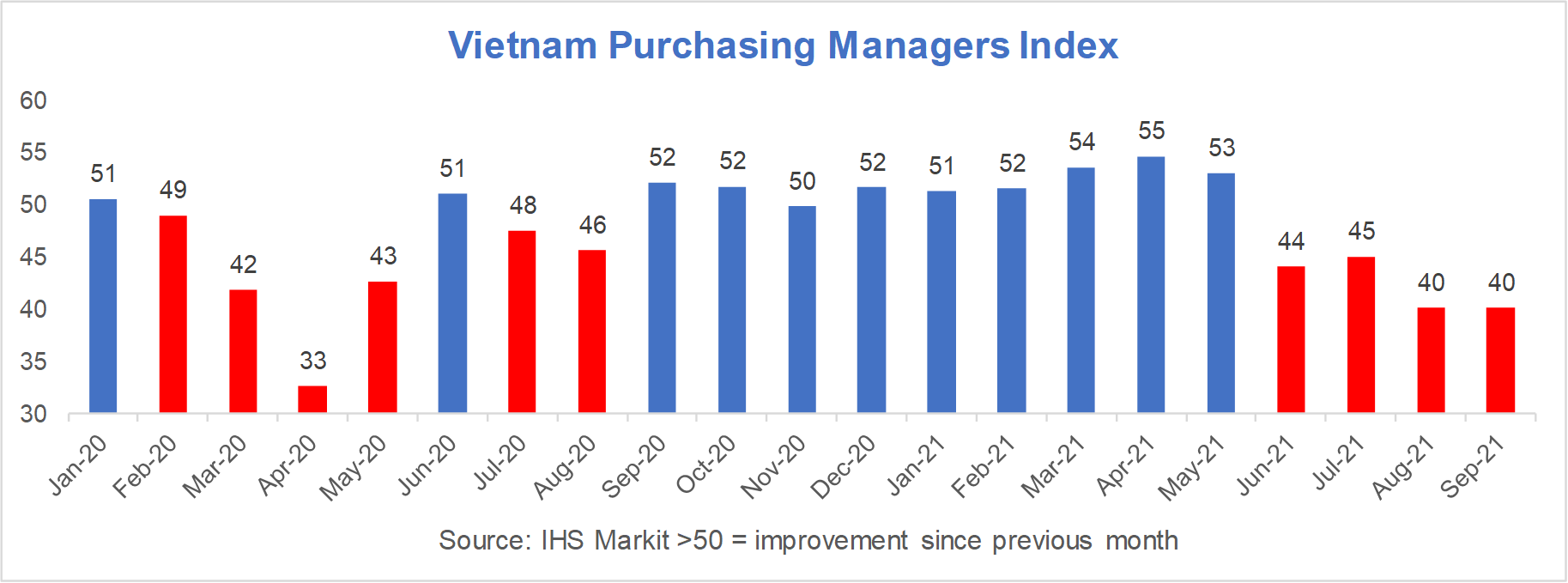

The Vietnam manufacturing purchasing managers index highlights the impact on one important sector which accounts for nearly one-quarter of GDP. As the indices drop below 50 a decline and as production output is experienced. The main index demonstrates the hit to production over the past four months.

Other indices with September 2021 indices shown in parenthesis show low output (28), logistic issues with supplier delivery times (29) and far fewer workers employed (38 – the lowest ever). Backlogs of work are building (60) and input prices are rising (66).

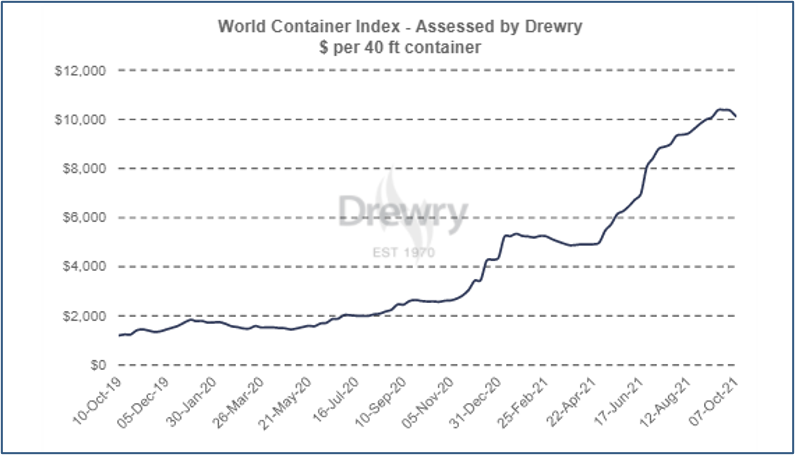

The recovery in 2020 was fast. In 2021 navigating Vietnam’s economic recovery post-Covid will be hampered by a lack of confidence, the ability to return to full capacity in ongoing social distancing restrictions, logistics slowing the movement of goods between provinces, global shipping container supply shortages and hikes in shipping costs.

Many production workers migrate to production hubs (approximately 3,500,000 workers migrate to HCMC, Dong Nai, Binh Duong and Long An), when many lost their jobs during the lockdown, they were unable to return to their homes in the provinces, often small towns and rural areas. These families experienced extreme hardships and anxiety from a combination of no income to cover daily necessities and Covid concerns.

Many workers desire to go home to the safety and stability afforded by their provincial family homes. The agricultural economy acts as a sponge to this workforce, they have shelter, can eat, but are grossly underemployed. As the lockdown restrictions have eased many have left and others are waiting to return home.

Getting them to come back to production hubs again before Tet (lunar new year) in late January 2021 will be difficult. Harvest is fast approaching for many communities with rice sowing expected in the Mekong Delta in November and December and coffee harvest expected in October in the Central Highlands.

For these migrant workers particularly and consumers generally, confidence is extremely low with an absolute fall of over 60% compared to 2019. Building confidence is critical to navigating Vietnam’s economic recovery post-Covid and attracting people back to work and to encouraging consumer spending. Some key factors to encourage consumer confidence include;

Visit AskCimigo and interrogate the report with our AI assistant.

Get instant access to syndicated consumer insights, market trends, and competitive intelligence across Vietnam.

The economic impact of Covid is unprecedented in peacetime, the impact in 2021 is a much harder impact than 2020. Navigating Vietnam’s economic recovery post-Covid in 2021 and beyond will be far harder than experiences to date. Cimigo estimates that 1.6 million jobs were lost in 2020 compared to 5.9 million lost in 2021. Many employees and micro and SME business owners have lost significant levels of income through salary reduction and revenue declines respectively. Cimigo estimate that household incomes diminished by 12% in 2020 and forecast that they will diminish by 38% in 2021.

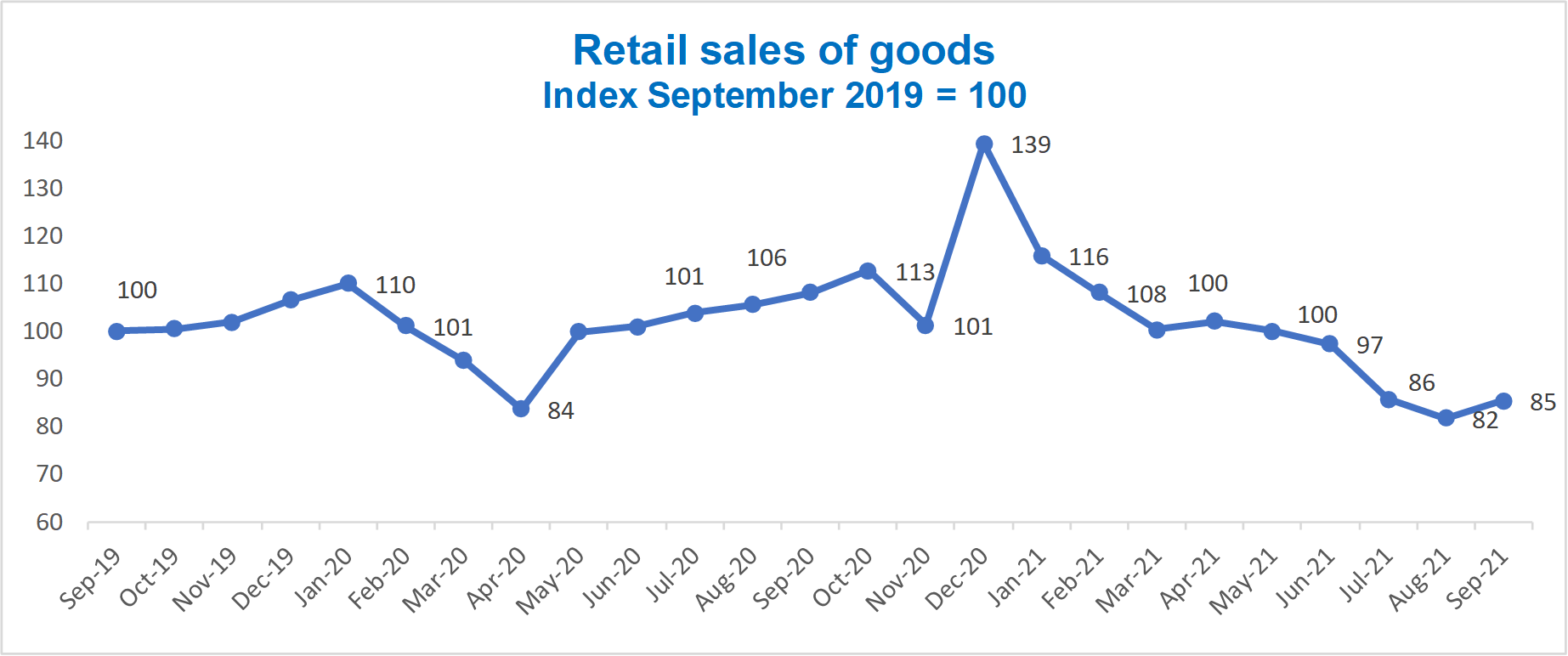

Vietnam retail sales react quickly to lockdowns and lower-income levels. The chart below shows monthly retail sales of goods (not services) indexed against September 2019 at 100.

Vietnam retail sales of goods recovered quickly after the 2020 lockdown but did not have the time to build the momentum of growth experienced in 2018 (15% year on year) and 2019 (12% year on year) growth.

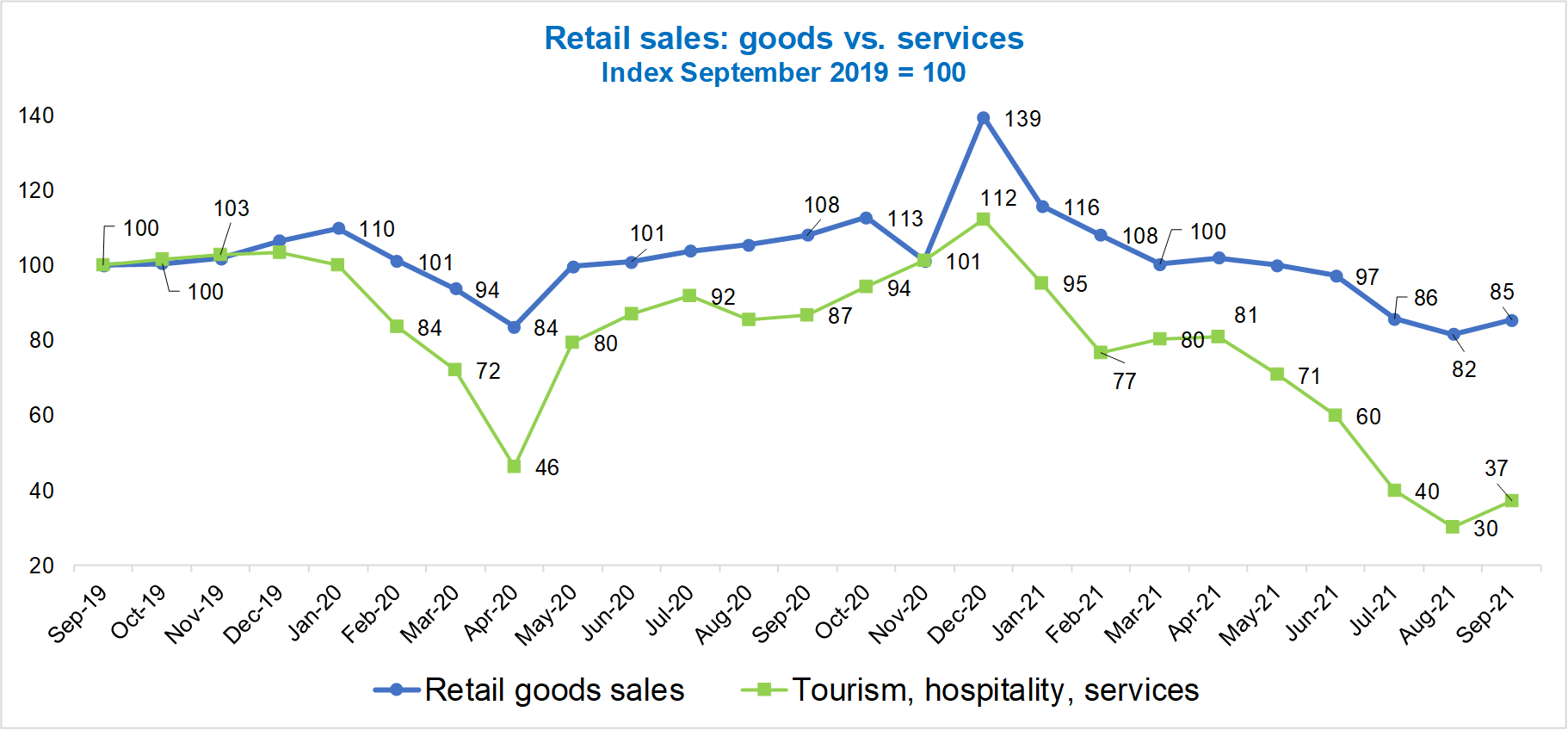

Vietnam retail sales of services have been hit far harder. This includes tourism, hospitality and other services. In absolute terms, pre-pandemic retail services equate to 30% of the value of retail goods sales.

The chart below shows monthly retail sales of goods versus services, indexed against September 2019 at 100.

Services never truly bounced back from the pandemic experience in 2020 and have taken a severe hit in 2021. Restrictions preventing travel and closing hospitality and many other services explain the impact but the rebound is far harder to achieve because many such services are discretionary and not essential household expenses.

Cimigo does not expect a return to 2019 pre-pandemic expenditure levels for 18 to 24 months after these services are allowed to re-open and operate normally. Rebuilding consumer confidence will be key to encouraging discretionary expenditure. In 2019 discretionary expenditure accounted for 33% of all household expenditure.

TET is a time for renewal, celebration and connecting with family in Vietnam. TET is a huge financial burden to household budgets in gifting, food and beverages to serve to guests and premiumisation of the brands used.

TET is an important consumption occasion for many categories locking in near 30% of annual sales in just 6 weeks. TET will see subdued expenditure in pre-TET hospitality, grocery spending and gifting. The impact on retailers and many consumer-packaged goods companies will prevent growth in 2022.

The categories depicted below saw a contraction of sales in 2020 and 2021. The decline is more marked for those to the left of the chart below. Outbound travel, out-of-home entertainment, domestic travel, eating out of home, spa and beauty services all experienced massive declines in demand.

High ticket vehicles and durables suffered as purchases are delayed. New apartment sales, cars, home appliances are goods that consumers defer purchases until such time that their confidence rebounds.

In contrast, the categories and channels depicted below saw their historic growth accelerate (often dramatically) in 2020 and their momentum continues in 2021. The growth is more marked for those to the left of the chart below.

Those categories and channels above the arrow will see their growth endure, spurred forward by Covid and fundamentally altering how consumers in Vietnam behave. These changes in behaviour will not reverse as Covid dissipates. Those categories below the arrow are shifts in consumer expenditure that will not endure, as they are reactionary behavioural changes brought about by Covid.

Consumer confidence has hit new lows, businesses have faltered, jobs have been lost and incomes reduced. Many sectors will remain distressed, especially tourism, the airline, leisure and hospitality industry.

Disposable incomes have been severely impacted and uncertainly will reign at the forefront of consumer minds. Spending beyond necessities will remain suspended. Greater value will be sought across household expenditures.

Vietnamese consumers will trade down their brand choices to save money. Consumers will shop more frequently but in smaller quantities. They will seek to conserve cash in their pockets. Cash outlay will trump price sensitivity. A minority of affluent consumers will seek value in bulk, multi-serve and large pack purchases.

Vietnamese consumers will seek lower-cost channels. They will go out of their way to find better prices and Vietnamese consumers will pay greater attention to promotions. To protect your brand whilst providing value in your promotions, is a tough balancing act.

Retail sales in Vietnam grew 12% in 2018, 15% in 2019 and just 2.6% in 2020. Consumer spending will only return to pre-pandemic 2019 growth levels after 18 to 24 months. This pandemic will force a sharp drop in discretionary expenditure. In Vietnam during 2019 (pre-pandemic) 33% of household expenditure was on discretionary items.

There will be a GDP growth of approximately 2.4% in 2021. This is the lowest level since 1986 which recorded a 2.3% growth. It will be less than 2020 which recorded a 2.9% growth and in sharp contrast to the 7.0% growth achieved in 2019.

By mid-2023, Vietnam will witness consumer dynamism and economic growth rebound unabated. The pace of positive economic progress and consumer dynamism will return to the level seen in 2019, then quicken and outpace other developing markets.

Visit AskCimigo and interrogate the report with our AI assistant.

Get instant access to syndicated consumer insights, market trends, and competitive intelligence across Vietnam.

If you have any questions or specific needs, please get in touch with us at ask@cimigo.com.

Vietnam Q1 2026 economic outlook

May 11, 2026

Vietnam Q1 2026 economic outlook: strong growth, rising pressure, falling confidence Vietnam Q1

Vietnam outlook: CEOs turn sharply pessimistic

Apr 21, 2026

CEOs turn sharply pessimistic as pressures intensify in Q1 2026. The Vietnam outlook among CEOs in

The informed consumer era: how independent research is redefining Indonesian fintech

Apr 17, 2026

The Indonesian fintech (financial technology) landscape has undergone a seismic shift. Digital

Đoàn Ngọc Huy (Johnny Doan), CMO & Market Research Expert -

As a Marketing Director and Market Research Expert Advisor across international markets, I have collaborated with numerous market research agencies, both global and local, that operate with a high level of professionalism and effectiveness. Cimigo is among the most outstanding. The Cimigo team demonstrates exceptional professionalism, strong commitment, and operational excellence. From research design and fieldwork execution to insight analysis, all stages are conducted rigorously, delivered on schedule, and closely aligned with business objectives. This is a highly capable team that I would confidently recommend to my partners and stakeholders.

As a Marketing Director and Market Research Expert Advisor across international markets, I have collaborated with numerous market research agencies, both global and local, that operate with a high level of professionalism and effectiveness. Cimigo is among the most outstanding. The Cimigo team demonstrates exceptional professionalism, strong commitment, and operational excellence. From research design and fieldwork execution to insight analysis, all stages are conducted rigorously, delivered on schedule, and closely aligned with business objectives. This is a highly capable team that I would confidently recommend to my partners and stakeholders.

Lisa Nguyen - Vietnam Marketing Lead

Mark Ratcliff - Managing Director

The team at Cimigo are my favourite researchers in South East Asia. They’ve proved adept at tackling the most private and complex personal issues at qualitative research level, not flinching when the client endlessly chopped and changed fieldwork timing, or ramped up the workload without warning. They have recruited the most extraordinarily niche consumers without pause or complaint. Their patience with clients and their flexibility and hard work that went above and beyond what was initially asked of them on two projects relating to sexual behaviour means there is now no other research company we would choose to work with in that part of Asia. The fact they also pulled off a third project for us so well, on men’s relationship with beer and beer advertising, shows they have breadth of expertise— we still quote from the report they produced.

The team at Cimigo are my favourite researchers in South East Asia. They’ve proved adept at tackling the most private and complex personal issues at qualitative research level, not flinching when the client endlessly chopped and changed fieldwork timing, or ramped up the workload without warning. They have recruited the most extraordinarily niche consumers without pause or complaint. Their patience with clients and their flexibility and hard work that went above and beyond what was initially asked of them on two projects relating to sexual behaviour means there is now no other research company we would choose to work with in that part of Asia. The fact they also pulled off a third project for us so well, on men’s relationship with beer and beer advertising, shows they have breadth of expertise— we still quote from the report they produced.

Kevin McQuillan - Chief Marketing Officer

Sam Houston - Chief Executive Officer

Minh Thu - Consumer Market Insights Manager

Travis Mitchell - Executive Director

Malcolm Farmer - Managing Director

Hy Vu - Head of Research Department

Joe Nelson - New Zealand Consulate General

Steve Kretschmer - Executive Director

York Spencer - Global Marketing Director

Laura Baines - Programmes Snr Manager

Mai Trang - Brand Manager of Romano

Hanh Dang - Product Marketing Manager

Luan Nguyen - Market Research Team Leader

Max Lee - Project Manager

Chris Elkin - Founder

Ronald Reagan - Deputy Group Head After Sales & CS Operation

Chad Ovel - Partner

Private English Language Schools - Chief Executive Officer

Rick Reid - Creative Director

Anya Nipper - Project Coordination Director

Dr. Jean-Marcel Guillon - Chief Executive Officer

Joyce - Pricing Manager

Matt Thwaites - Commercial Director

Aashish Kapoor - Head of Marketing

Kelly Vo - Founder & Host

Thanyachat Auttanukune - Board of Management

Hamish Glendinning - Business Lead

Thuy Le - Consumer Insight Manager

Richard Willis - Director

Ha Dinh - Project Lead

Geert Heestermans - Marketing Director

Vo Thi Thuy Ha - Commercial Effectiveness

Louise Knox - Consumer Technical Insights

Aimee Shear - Senior Research Executive

Dennis Kurnia - Head of Consumer Insights

Tania Desela - Senior Product Manager

Thu Phung - CTI Manager

Linda Yeoh - CMI Manager

Cimigo’s market research team in Vietnam and Indonesia love to help you make better choices.

Cimigo provides market research solutions in Vietnam and Indonesia that will help you make better choices.

Cimigo provides a range of consumer marketing trends and market research on market sectors and consumer segments in Vietnam and Indonesia.

Cimigo provides a range of free market research reports on market sectors and consumer segments in Vietnam and Indonesia.