Indonesia’s economy 2024

Feb 28, 2025

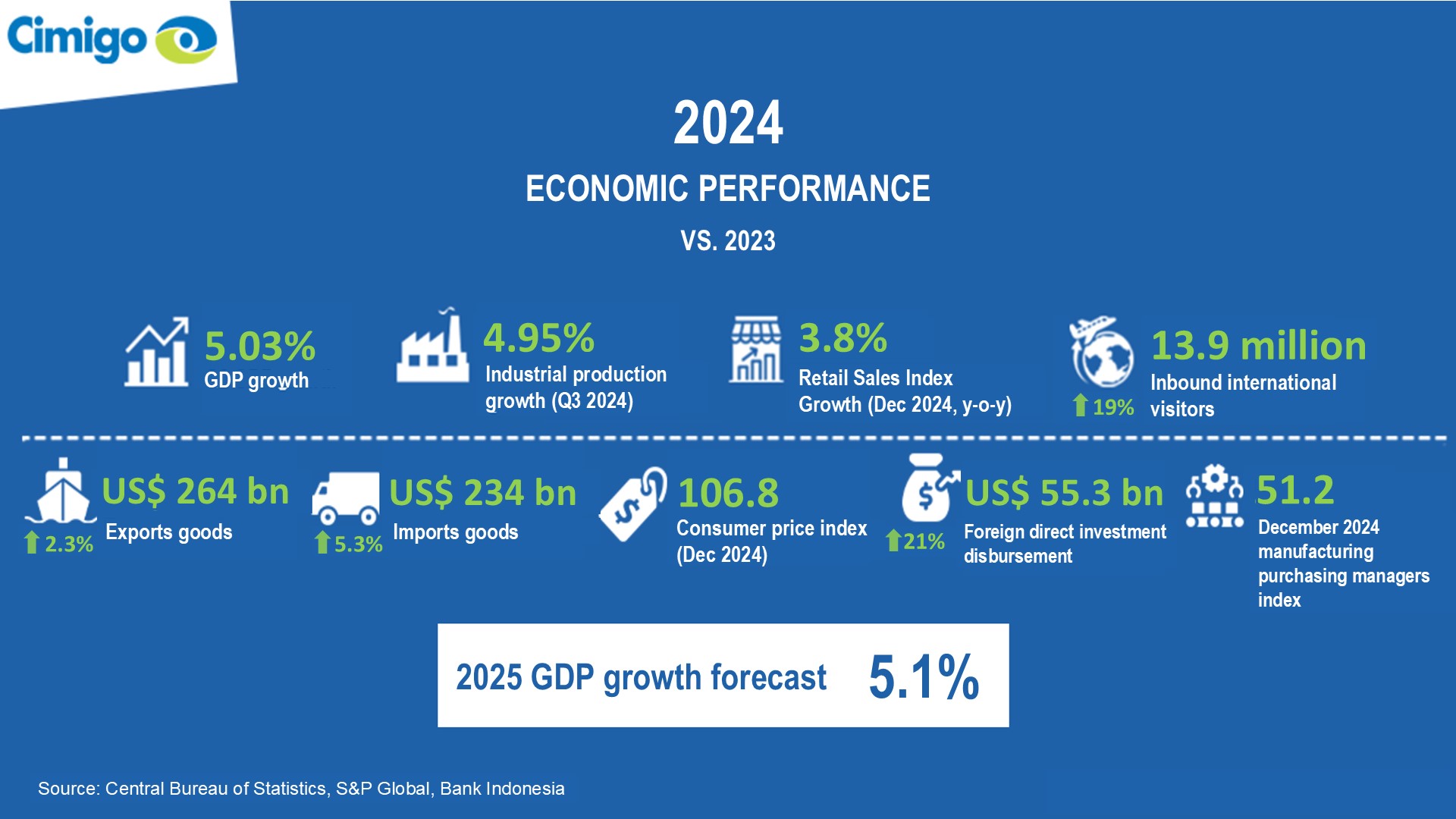

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

Vietnam retail banking

Vietnam retail banking has great potential and has become very competitive. With middle-class acceleration and lower birth rates, households are smaller and have become wealthier. Vietnam has experienced a rapid rise in modern retail trade and e-commerce which promote non-cash payments. Non-cash payment is growing at a rapid pace via online, mobile wallets, mobile banking and QR codes.

Vietnam retail banking has great potential and has become very competitive. With middle-class acceleration and lower birth rates, households are smaller and have become wealthier. Vietnam has experienced a rapid rise in modern retail trade and e-commerce which promote non-cash payments. Non-cash payment is growing at a rapid pace via online, mobile wallets, mobile banking and QR codes.

According to the State Bank*, in the first haft of 2022 compared to the same period of 2021, non-cash transactions increased 77% in volume and 30% in value. The same period experienced increases of; 63% (volume) and 32% (value) for internet banking, 98% (volume) and 84% (value) for mobile transactions and 86% (volume) and 127% (value) for QR code payments.

In 2021, retail loans accounted for 40-50% of bank loans. Retail banking is a trust-based customer-oriented business. Brand image, customer experience and customer journey play critical roles in any bank’s competitive position. Cimigo’s Vietnam retail banking 2022 report provides intelligence on banks’ competitive position. This is essential for both managing communications and driving operational improvements.

The survey included 2,055 interviews nationwide. The targeted respondents are aged 18 – 55 years and have a bank account. The sample covers key cities (Hanoi, HCMC, Danang, Hai Phong and Can Tho) and both urban and rural strata in other provinces with respondent profiles in proportion to the population’s demographic profile.

The Vietnam retail banking report is available to download for free. Customised reports with analysis specific to your bank relative to your strategies and target retail banking customers are available for a fee of VND120,000,000 (US$5,000).

Download the Vietnam retail banking report here

The Vietnamese retail banking market is dominated by state-owned commercial banks. This is driven by physical accessibility, especially beyond the key cities of Hanoi, HCMC, Danang, Hai Phong and Can Tho. Retail banking in Vietnam has great growth potential and is experiencing dynamic competition with other non-bank financial firms.

The top banks in Vietnam deliver good customer experience whilst strong brand building is nascent. Techcombank performs strongly in both brand building and customer experience. The rise in non-cash payments, modern trade and e-commerce in Vietnam means that digital transformation will continue to change the shape of the Vietnamese retail banking sector. Improving Vietnamese customers’ digital experience and the ecosystem of digital products and services is key to future success.

Cimigo expects Vietnam’s gross domestic product to grow 7.4% in the full year 2022. The Vietnamese banking sector has gone through an eventful 2021 given the impact of COVID-19. Although risks and uncertainty remain the sector has benefited from a strong economic recovery, government support for non-cash payments and increasing digital transformation. Most banks reported impressive profits in Q1 and Q2 2022.

Leading state-owned banks dominate the traditional transaction point network (ATMs, transaction offices and branches). These banks hold long-term competitive advantages derived from their network, trustworthiness and high popularity. They perform well in salience, usage and market share for the most frequently used bank. However, their customer experience metric, net promoter score (NPS), underperforms the average of the top 10 banks (BIDV is the one exception).

Amongst the private joint stock commercial banks, the transaction point network is not a competitive advantage. According to the Ministry of Culture, Sports and Tourism*, only TPBank which currently has the smallest physical network, amongst the top 10 banks, continue to invest significantly in expanding their transaction point network.

Download the Vietnam retail banking report here

In the key cities of Hanoi, HCMC, Danang, Hai Phong and Can Tho both transaction values and customer expectations are greater. Techcombank demonstrates an impressive performance in these cities, surpassing both Agribank and Vietinbank to compete closely with BIDV and MBbank. Techcombank gains the highest usage share in Hanoi. Both ACB and Sacombank perform significantly better in HCMC than they do nationally. In fact, in HCMC the market is more dynamic with smaller banks achieving a share of use than seen in Hanoi. The top 10 retail banks in Vietnam achieve more than 90% share of bank usage across products.

Switching banks for a customer is complicated and time-consuming. Once a new bank has been tried, conversion to the most used bank is high. Easing the customer process to opening a bank is the key barrier for banks to overcome in order to improve their performance.

Across all financial products; term deposits, business loans, house loans and health insurance have the most potential for growth.

Retail banking experienced increased competition from various financial firms including; consumer finance, e-wallets, digital lending, personal finance investment, insurance tech, credit scoring and buy now pay later (BNPL) firms. These other financial firms focus on mass consumers with their simple processes, digital journeys and micro products. They are growing and attracted funding of an estimated US$1.3 billion in 2021.

18% of bank customers use other products (excluding e-wallets) provided by non-bank firms. This indicates a high demand for financial products and raises an opportunity for retail banks to encourage their current customers to use more banking products.

TPBank, ACB, Techcombank, Sacombank, BIDV and MBbank are all considered excellent. Net promoter score (NPS) is a widely used market research metric that is based on a single survey question asking respondents to rate the likelihood that they would recommend their bank to a friend. The NPS is typically interpreted and used as an indicator of customer loyalty as well as relative brand growth within an industry.

The top 10 banks record a high NPS (74 on average). Vietcombank, Agribank and Vietinbank are strong banks but need to put more effort to improve their customer experience as they underperform the average of the top 10 banks. The leading banks are doing well in bank staff, facilities and customer services.

Fees and quality of products and services impact NPS the most. The top banks receive high satisfaction on these factors. However, online products and services, efficient processes and procedures are key NPS drivers which still have vast room for improvement. Note that branches and ATM networks cease to be a priority in recommending a bank as digital banking takes hold.

Download the Vietnam retail banking report here

Non-state-owned banks perform better on their customer experience metric net promoter score (NPS). MBbank and Techcombank have significantly better brand performance in the key cities of Hanoi, HCMC, Danang, Hai Phong and Can Tho. These two brands also have the highest share of usage for stock trading and their share of digital banking services is comparable to that of the state-owned banks.

In terms of communication and brand building, all brands exhibit limited performance except Techcombank. Techcombank’s brand-building efforts show a positive impact as it is strongly associated with core factors that impact to the overall bank appeal such as being recommended, good customer experience, good products and is widely used.

Some banks have chosen to create their own fully digital banks, such as; CAKE, TIMO, TNEX and OCTO.

Physical accessibility is the most common reason for using a bank most often. However to drive appeal to the bank and motivate customer acquisition banks will need to focus on customer experience which will promote recommendations. Cimigo expects that physical accessibility will play a lesser role in bank performance going forward.

The quality of mobile banking applications and online services is a key reason to use a bank and a driver for the customer experience metric net promoter score (NPS). Banks are investing to digitalise their products and services as a core strategy to compete for retail banking customers.

Four in ten retail banking customers are using e-wallets which are very strong for their user experience, eco-system and promotions. E-wallet users need to link their e-wallet to their bank account, which raises an opportunity for banks to leverage e-wallets as a bridge to increase their saliency and usage. The top banks keep improving their current mobile application by integrating various products and features.

As an alternate strategy, some banks have launched all new brands for their digital bank (a new form of banking that digitises all the activities and services). Micro products, ecosystems and personal financial management tools are being promoted as the key triggers to attract customers.

Instead of expanding physical accessibility, digital banking is a more efficient solution to simplify processes, develop micro products and encourage customer recruitment for retail banks.

As an example Cake (powered by VPbank in cooperation with Be Group) claim an impressive number of users (more than 2 million). Big data and AI technology provide an advantage to support digital banks to offer the most suitable products to customers as well as more efficient credit risk management. Building trustworthiness and overcoming concerns with cyber risks are the biggest barriers to overcome for digital banks.

To foster awareness beyond physical accessibility, social media, e-wallet and e-commerce platform linkage are the key sources. Acquiring customers beyond the key cities of Hanoi, HCMC, Danang, Hai Phong and Can Tho requires significant resources in communication and currently (although Cimigo expects this to dissipate rapidly) expanding branches and ATMs networks.

Trustworthy image, simple process and procedure need to be highlighted in communication and delivered throughout customer journeys. In the key cities where customers less rely on physical accessibility and customer experience is more important, banks should prioritise resources to improve their customer experience to generate recommendations and build trust. Digital transformation is changing retail banking dynamics. Improving customers’ digital experience and the ecosystem of digital products and services is key.

Download the Vietnam retail banking report here

End.

Indonesia’s economy 2024

Feb 28, 2025

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

Vietnam consumer trends 2025

Feb 23, 2025

Vietnam consumer trends 2025 Vietnam consumer trends 2025 explores the eight reasons Vietnam will

Beyond beauty: The changing face of personal care in Indonesia

Jan 27, 2025

The personal care market in Indonesia is undergoing a significant transformation, with consumers

Lisa Nguyen - VN Marketing Lead

Sam Houston - Chief Executive Officer

Minh Thu - Consumer Market Insights Manager

Travis Mitchell - Executive Director

Malcolm Farmer - Managing Director

Hy Vu - Head of Research Department

Joe Nelson - New Zealand Consulate General

Steve Kretschmer - Executive Director

York Spencer - Global Marketing Director

Laura Baines - Programmes Snr Manager

Mai Trang - Brand Manager of Romano

Hanh Dang - Product Marketing Manager

Luan Nguyen - Market Research Team Leader

Max Lee - Project Manager

Chris Elkin - Founder

Ronald Reagan - Deputy Group Head After Sales & CS Operation

Chad Ovel - Partner

Private English Language Schools - Chief Executive Officer

Rick Reid - Creative Director

Janine Katzberg - Projects Director

Anya Nipper - Project Coordination Director

Dr. Jean-Marcel Guillon - Chief Executive Officer

Joyce - Pricing Manager

Matt Thwaites - Commercial Director

Aashish Kapoor - Head of Marketing

Kelly Vo - Founder & Host

Thanyachat Auttanukune - Board of Management

Hamish Glendinning - Business Lead

Thuy Le - Consumer Insight Manager

Richard Willis - Director

Ha Dinh - Project Lead

Geert Heestermans - Marketing Director

Louise Knox - Consumer Technical Insights

Aimee Shear - Senior Research Executive

Dennis Kurnia - Head of Consumer Insights

Tania Desela - Senior Product Manager

Thu Phung - CTI Manager

Linda Yeoh - CMI Manager

Cimigo’s market research team in Vietnam and Indonesia love to help you make better choices.

Cimigo provides market research solutions in Vietnam and Indonesia that will help you make better choices.

Cimigo provides a range of consumer marketing trends and market research on market sectors and consumer segments in Vietnam and Indonesia.

Cimigo provides a range of free market research reports on market sectors and consumer segments in Vietnam and Indonesia.