Indonesia’s economy 2024

Feb 28, 2025

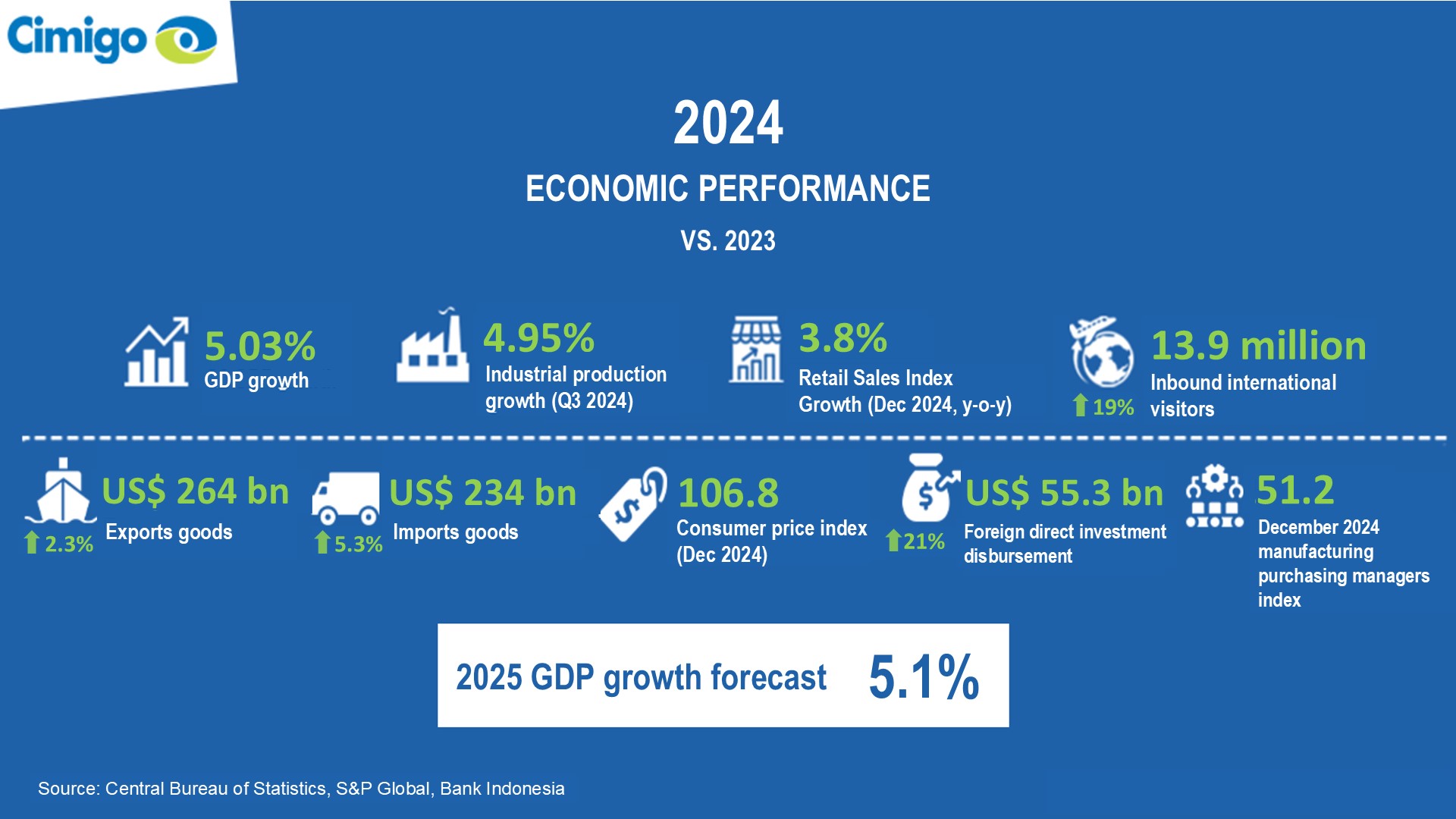

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

Vietnam retail banking 2024

Vietnam’s retail banking sector is in a transformative phase, with digital adoption accelerating as customer preferences evolve. Banks are not only competing with each other but also with new, agile, digital-only entrants that are reshaping how consumers interact with financial services. The Vietnam Retail Banking 2024 report from Cimigo reveals critical insights into this transformation, based on extensive customer research across key cities in Vietnam. This article highlights the main findings and provides strategic recommendations for banking institutions aiming to succeed in this dynamic environment. Digital transformation in Vietnamese banking

Digital payment methods dominate recent transactions in Vietnam, reflecting the widespread adoption of digital financial solutions. Bank apps lead as the most popular choice, with users primarily utilising them for linking to websites or e-commerce platforms and performing manual transfers. E-wallets closely follow, driven by similar functionality, including website integration and manual transfers. Together, bank apps and e-wallets represent the majority of payments, highlighting a clear shift away from traditional methods like bank cards and cash.

The competition amongst banks has intensified, with notable changes in market leadership. In a shift from previous years, MBBank has emerged as the market leader in 2024, overtaking Vietcombank, which traditionally held the top position. This change is significant, highlighting how digital initiatives and customer engagement strategies are increasingly influencing market dynamics.

Meanwhile, traditional players like BIDV, VietinBank, Agribank, and Sacombank are experiencing declines in their Brand Power Index (BPI). This decline suggests that these banks are struggling to adapt as effectively to new consumer expectations, particularly around digital services and customer experience.

At the same time, digital-only banks like CAKE by VPBank and TNEX have gained momentum and now ranked amongst the top 20 in brand power, illustrating the growing appeal of digital-first services. These banks leverage their lack of physical branches to provide convenient, mobile-centric experiences that resonate with younger, tech-savvy consumers. As these digital players grow in popularity, the competition is set to reshape Vietnam’s banking landscape further.

As digital technologies become integral to daily life, Vietnamese consumers increasingly prefer engaging with banks through digital channels. According to the report, online platforms, including social media and streaming services, are now the primary sources of banking information, surpassing traditional communication methods. This trend underscores a strong customer demand for digital convenience and access.

This shift presents an opportunity for banks to strengthen their digital presence. Social media, with a 52% engagement rate, has become a crucial platform for banks to communicate with customers, followed closely by streaming platforms at 33%. These channels allow banks to interact with customers in a more personalised and accessible way, aligning with the needs of Vietnam’s growing middle class and young, digitally inclined population.

Traditional methods, such as ATM networks and word-of-mouth referrals, still play a role but are being overshadowed by the ease and immediacy of digital platforms. The report shows that an effective digital communication strategy, supported by mobile apps and optimised websites, will be essential for banks aiming to meet customers where they are. Digital transformation

Over half of Vietnamese retail banking customers use three or more banking products, and a significant number engage with multiple banks. This trend toward multi-product usage signals a more financially savvy consumer base that values variety and flexibility. Customers are increasingly looking for diverse financial solutions within a single banking ecosystem, which can help them manage different aspects of their financial lives whether saving, borrowing, or investing.

The report categorises customers into low and high-engagement groups based on their product usage. High-engagement customers who use multiple financial products and services represent a lucrative segment for banks aiming to grow their share of wallets. Targeted strategies that offer bundled services, loyalty rewards, or enhanced benefits can help banks strengthen relationships with this high-value segment.

Term deposits and savings accounts are top choices for Vietnamese consumers, reflecting a cautious financial approach amid economic uncertainties. These products provide the stability that many customers seek, especially during economic volatility. Demand deposits also hold steady appeal, while credit cards are on the rise, especially amongst younger, urban customers who prioritise flexibility in managing finances. The report suggests that as credit card usage expands, it may also signal increased financial pressure on consumers, particularly if they are using credit to manage daily expenses rather than for planned, larger purchases.

Banks that perform well on the Brand Power Index (BPI) enjoy higher levels of brand loyalty and customer retention. MBBank and Vietcombank lead in both brand awareness and customer conversion, with MBBank also achieving the highest Net Promoter Score (NPS) in the market. This indicates that customers are not only aware of MBBank but also see it as a reliable and trustworthy primary banking partner.

However, challenges remain for some brands. For instance, VPBank, despite high brand awareness, struggles to convert occasional users into loyal customers who use VPBank as their primary banking institution. Similarly, CAKE and Timo, whilst building strong reputations as digital-first banks, have yet to convert many of their customers into loyal, primary users. This demonstrates that awareness alone is not enough; banks must also focus on deepening customer relationships and meeting evolving needs.

Digital-first banks like CAKE and TNEX are popular amongst younger consumers, with an emphasis on convenience, ease of use, and mobile accessibility. They are carving out niches within the market, appealing especially to younger demographics that are less likely to visit physical branches and more inclined to manage their finances digitally. Digital transformation

Regional and demographic preferences vary significantly. MBBank is especially strong in the Mekong Delta and the North, whilst Vietcombank remains the leader in the urban hub of Ho Chi Minh City.

To keep up with rapidly increasing digital demands, banks must prioritise their digital offerings. Key areas for improvement include:

Investing in secure, user-friendly mobile banking options is essential. Digital enhancements will not only improve customer satisfaction but also drive cost efficiencies by reducing reliance on physical branches. Digital transformation

As customers embrace multiple financial products, banks have an opportunity to offer cross-selling packages tailored to different customer segments. For instance:

By aligning product bundles with customer demographics and usage patterns, banks can deepen customer relationships and enhance lifetime value.

Customer experience remains a core differentiator in Vietnam’s retail banking sector. Banks that excel in key areas—such as service quality, staff competence, and efficient transaction processes—are better positioned to earn customer loyalty and high NPS ratings. Banks should continually monitor customer satisfaction and identify areas for improvement, especially given the intense competition from digital-first players that often offer streamlined, user-centric experiences.

Vietnamese consumers’ interest in stable savings products and flexible credit options highlights the need for innovation in these areas. By developing flexible term deposits with varied interest terms or launching secure online credit options, banks can cater to customers seeking a mix of stability and convenience. Offering such products digitally will also help banks reach a broader customer base, including younger users who prioritise mobile accessibility.

Vietnam’s retail banking industry is at a critical juncture, with digital transformation in Vietnamese banking shaping the sector’s future. To thrive in this evolving landscape, banks must embrace digital innovation, enhance customer experience, and tailor their offerings to meet specific demographic needs. Strategic agility and a commitment to customer-centric solutions are essential for banks aiming to succeed as digital competition intensifies and customer expectations continue to grow. By addressing these priorities, banks can strengthen their market position and foster long-term customer loyalty in 2025 and beyond.

Cimigo Vietnam Retail Banking report is now available for purchase and can be tailored to your specific needs. Pricing starts at VND 60,000,000. If you would like further details, email us at ask@cimigo.com.

End.

Indonesia’s economy 2024

Feb 28, 2025

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

Vietnam consumer trends 2025

Feb 23, 2025

Vietnam consumer trends 2025 Vietnam consumer trends 2025 explores the eight reasons Vietnam will

Beyond beauty: The changing face of personal care in Indonesia

Jan 27, 2025

The personal care market in Indonesia is undergoing a significant transformation, with consumers

Lisa Nguyen - VN Marketing Lead

Sam Houston - Chief Executive Officer

Minh Thu - Consumer Market Insights Manager

Travis Mitchell - Executive Director

Malcolm Farmer - Managing Director

Hy Vu - Head of Research Department

Joe Nelson - New Zealand Consulate General

Steve Kretschmer - Executive Director

York Spencer - Global Marketing Director

Laura Baines - Programmes Snr Manager

Mai Trang - Brand Manager of Romano

Hanh Dang - Product Marketing Manager

Luan Nguyen - Market Research Team Leader

Max Lee - Project Manager

Chris Elkin - Founder

Ronald Reagan - Deputy Group Head After Sales & CS Operation

Chad Ovel - Partner

Private English Language Schools - Chief Executive Officer

Rick Reid - Creative Director

Janine Katzberg - Projects Director

Anya Nipper - Project Coordination Director

Dr. Jean-Marcel Guillon - Chief Executive Officer

Joyce - Pricing Manager

Matt Thwaites - Commercial Director

Aashish Kapoor - Head of Marketing

Kelly Vo - Founder & Host

Thanyachat Auttanukune - Board of Management

Hamish Glendinning - Business Lead

Thuy Le - Consumer Insight Manager

Richard Willis - Director

Ha Dinh - Project Lead

Geert Heestermans - Marketing Director

Louise Knox - Consumer Technical Insights

Aimee Shear - Senior Research Executive

Dennis Kurnia - Head of Consumer Insights

Tania Desela - Senior Product Manager

Thu Phung - CTI Manager

Linda Yeoh - CMI Manager

Cimigo’s market research team in Vietnam and Indonesia love to help you make better choices.

Cimigo provides market research solutions in Vietnam and Indonesia that will help you make better choices.

Cimigo provides a range of consumer marketing trends and market research on market sectors and consumer segments in Vietnam and Indonesia.

Cimigo provides a range of free market research reports on market sectors and consumer segments in Vietnam and Indonesia.