Indonesia’s economy 2024

Feb 28, 2025

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

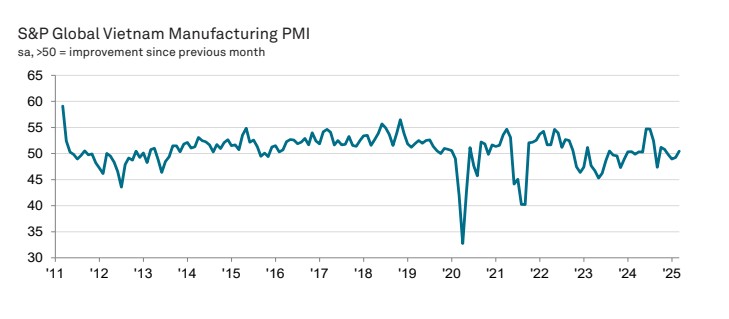

Vietnam PMI March 2025 – manufacturing purchasing managers index

Cimigo Vietnam market research has collected the Vietnam PMI – manufacturing purchasing managers index since 2013. S&P Global compiles the Vietnam PMI S&P Global from responses to monthly questionnaires sent to purchasing managers in a panel of around 400 manufacturers.

The Vietnamese manufacturing sector returned to growth in March amid renewed increases in both output and total new orders. That said, international demand weakened, and firms were cautious around hiring and purchasing as business confidence softened. Meanwhile, the rate of input cost inflation eased and manufacturers lowered their selling prices for the third month running.

The S&P Global Vietnam Manufacturing Purchasing Managers’ Index™ (PMI®) posted above the 50.0 no-change mark for the first time in four months during March, thereby signalling an improvement in business conditions at the end of the first quarter of 2025. At 50.5, the PMI was up from 49.2 in February and pointed to a slight strengthening in the health of the sector.

Manufacturing production increased for the first time in three months during March, and to the largest degree since August last year. According to respondents, the rise in output in part reflected improvements in the availability of goods, but also a renewed increase in new orders, which likewise expanded following a two-month sequence of decline.

Growth of new orders was recorded amid signs of improving customer demand, but was only slight amid ongoing weakness in international demand. In fact, new export orders decreased markedly and at the fastest pace since July 2023. New business from abroad has now fallen in five successive months. Some panellists reported a drop in orders from Mainland China.

While output and total new orders returned to growth, firms were slightly less confident in the year- head outlook for production than was the case in February. Sentiment remained positive amid higher new orders and hopes for stable demand, but optimism was below the series average.

Manufacturers exhibited caution with regards to employment and purchasing in March. Staffing levels decreased for the sixth consecutive month, linked to a recent period of subdued demand and staff resignations. That said, the drop in workforce numbers was the weakest in 2025 so far.

Purchasing activity, meanwhile, decreased for the first time in four months, with firms suggesting that the recent period of input buying meant that holdings of goods were sufficient to support output requirements. In turn, stocks of purchases decreased, albeit to the least marked extent since August last year. Stocks of finished goods were also down amid some reports that firms were reluctant to hold excess inventories.

Where firms did purchase inputs, they were faced with a further lengthening of suppliers’ delivery times, often linked to delays receiving goods from abroad. That said, the latest deterioration in vendor performance was much less pronounced than that seen in February and the weakest in seven months. Some panellists reported better stock availability at suppliers and faster transportation.

While higher costs for some imported items led input prices to increase again in March, muted demand for inputs led some suppliers to reduce their prices. Overall, input costs increased only slightly and at the slowest pace in the current 20-month sequence of inflation. Meanwhile, efforts to maintain competitiveness led manufacturers in Vietnam to lower their selling prices for the third consecutive month. The fall was only slight, however.

Approach

The S&P Global Vietnam Manufacturing PMI® is compiled by S&P Global from responses to monthly questionnaires sent to purchasing managers in a panel of around 400 manufacturers. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP.

Survey responses are collected by Cimigo Vietnam in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses.

The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

Indonesia’s economy 2024

Feb 28, 2025

Resilient growth amid challenges Indonesia’s economy continued to expand in 2024 despite global

Vietnam consumer trends 2025

Feb 23, 2025

Vietnam consumer trends 2025 Vietnam consumer trends 2025 explores the eight reasons Vietnam will

Beyond beauty: The changing face of personal care in Indonesia

Jan 27, 2025

The personal care market in Indonesia is undergoing a significant transformation, with consumers

Lisa Nguyen - VN Marketing Lead

Sam Houston - Chief Executive Officer

Minh Thu - Consumer Market Insights Manager

Travis Mitchell - Executive Director

Malcolm Farmer - Managing Director

Hy Vu - Head of Research Department

Joe Nelson - New Zealand Consulate General

Steve Kretschmer - Executive Director

York Spencer - Global Marketing Director

Laura Baines - Programmes Snr Manager

Mai Trang - Brand Manager of Romano

Hanh Dang - Product Marketing Manager

Luan Nguyen - Market Research Team Leader

Max Lee - Project Manager

Chris Elkin - Founder

Ronald Reagan - Deputy Group Head After Sales & CS Operation

Chad Ovel - Partner

Private English Language Schools - Chief Executive Officer

Rick Reid - Creative Director

Janine Katzberg - Projects Director

Anya Nipper - Project Coordination Director

Dr. Jean-Marcel Guillon - Chief Executive Officer

Joyce - Pricing Manager

Matt Thwaites - Commercial Director

Aashish Kapoor - Head of Marketing

Kelly Vo - Founder & Host

Thanyachat Auttanukune - Board of Management

Hamish Glendinning - Business Lead

Thuy Le - Consumer Insight Manager

Richard Willis - Director

Ha Dinh - Project Lead

Geert Heestermans - Marketing Director

Louise Knox - Consumer Technical Insights

Aimee Shear - Senior Research Executive

Dennis Kurnia - Head of Consumer Insights

Tania Desela - Senior Product Manager

Thu Phung - CTI Manager

Linda Yeoh - CMI Manager

Cimigo’s market research team in Vietnam and Indonesia love to help you make better choices.

Cimigo provides market research solutions in Vietnam and Indonesia that will help you make better choices.

Cimigo provides a range of consumer marketing trends and market research on market sectors and consumer segments in Vietnam and Indonesia.

Cimigo provides a range of free market research reports on market sectors and consumer segments in Vietnam and Indonesia.